Maradok

Maradok

Kereskedési feltételek

Products

Eszkozok

The EUR/USD is down more than 200 pips on Wednesday after several days of gains. It went from 1.0761 (four-week high) to 1.0517 (two-month low) in just a few hours. Such price dynamics are due to the general strengthening of the greenback: the U.S. dollar index is actively returning lost positions, reflecting the increased demand for the U.S. currency.

A logical question arises: why has the market so abruptly changed its mood? And can we talk about a "triumphant return" of the dollar, or are we dealing with a correction?

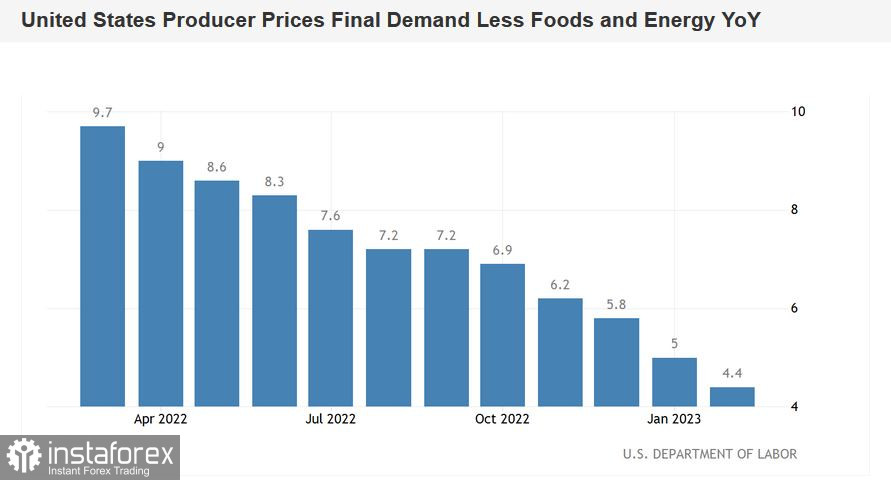

Inflation down, dollar up

It is noteworthy that the dollar strengthened on Wednesday amid the release of data on the U.S. Producer Price Index. The most important inflation report unexpectedly turned out to be in the "red", even despite very weak forecasts. U.S. annual PPI fell to 4.6% in February, with a forecast decline to 5.4%. The indicator has been consistently decreasing for 8 straight months. Taking out the often volatile food and energy components, core PPI also marked some declines: Annual price increases dropped to 4.4%, with a forecast of 5.2%. This indicator has been declining since April 2022.

Data on the volume of retail sales in the United States were also in the red. Excluding cars, the indicator turned out to be in the negative area, falling to -0.1%. The total volume decreased more significantly (-0.4%).

Another macroeconomic indicator also disappointed: the Empire State Manufacturing Index, which measures the level of general business conditions in the state of New York. It collapsed to -24 points, with a forecast decline to -7.9.

In other words, the reports published on Wednesday were clearly not on the dollar's side. Nevertheless, the US currency strengthened its positions in almost all pairs of the "major group" (except USD/JPY). Against the euro, the greenback was marked at 1.0517 (the low since January 6).

Such an unusual, at first glance, reaction from the dollar is due to several fundamental factors.

SVB and the Fed

After the collapse of Silicon Valley bank, and the subsequent bankruptcy of Signature Bank and Silvergate Capital Corp, rumors arose in the market that the Federal Reserve may refuse to raise interest rates at the March meeting (the results of which will be announced on March 22). Moreover, some experts voiced cautious assumptions about a possible step back in the context of a rate cut.

But today the situation has changed, primarily in the context of perception and interpretation of the events taking place. On the one hand, investors continue to sell off bank shares, and rating agencies Fitch and Moody's have worsened their forecast for the U.S. banking system. On the other hand, the opinion has crystallized in the foreign exchange market that the Fed will not pause in raising the rate, first of all, so as not to provoke a new wave of panic. Of course, you can forget about the 50-point scenario: if the Fed moves on, it will only be a quarter point hike.

An interesting fact: despite the "FOMC Blackout Period" (a 10-day period ahead of the meeting), a member of the Fed Board of Governors, Michelle Bowman, still commented on the current situation today. She did not say anything about monetary policy and economic prospects, but at the same time, noted that the banking system has strong capital and liquidity, remains stable and has a solid foundation. Thus, Bowman made it clear that the Fed will continue to focus on current tasks, primarily on combating high inflation.

It is worth noting that despite the slowdown in growth, the main inflation indicators are still at unacceptably high values. We have data on the Consumer Price Index and the PPI, while the Personal Consumption Expenditures Price Index will be published only on the last day of March, that is, after the Fed meeting. Indirect signs suggest that this inflation indicator (a key one for the Fed) may go back to rising: in February, the cost of air tickets, car insurance costs increased, prices for new cars increased. The rent for housing has also risen (after 5 months of decline).

In general, many factors suggest that the Fed will increase the rate by 25 points this month, thereby maintaining its previous pace.

Credit Suisse and the ECB

After initial emotions about the "bankfall" in the United States subsided, the market started to focus on the European banking sector. And, unfortunately, not without reason. We just found out that the shares of Credit Suisse (the second largest bank in Switzerland) fell by almost 30%. Stock trading has been halted several times by the stock exchange operator as volume has soared and stocks have plummeted. Investors reacted with hostility to the bank's report, in which it recognized the outflow of funds and "significant shortcomings" in the control of financial reporting. In addition, investors reacted negatively to the statement of the largest shareholder of Credit Suisse (National Bank of Saudi Arabia), which ruled out the possibility of providing additional assistance to the bank.

Amid such an information flow, the shares of European banks began to decline, and the dollar strengthened its position due to increased anti-risk sentiment.

Also, do not forget that this all happened before the European Central Bank's March meeting. Even before the situation with the Swiss bank, there was talk that the ECB could increase rates by only 25 points or even take a break. This forecast was published, in particular, by Deutsche Bank. The fall in Credit Suisse shares only added fuel to the fire, increasing pressure on the single currency.

Conclusions

The present fundamental background promotes the development of a downtrend for the EUR/USD pair. In the current situation, Credit Suisse may become a "black swan" for the bulls if the ECB doesn't risk to raise the interest rates on Thursday. The market focus has shifted from the problems of the American banks to the problems of the European banks. In this case, the dollar acts as a beneficiary, using the status of a protective asset.

From a technical point of view, the pair is below all the lines of the Ichimoku indicator and between the middle and the bottom lines of the BB indicator on the 1D chart. The pair is close to the support level of 1.0510 (lower line BB), and if EUR/USD breaks through this level, the bears will have a chance to reach the 4th figure. It is better to consider short positions after the bears sell from this level. In this case, the next price barrier will be 1.0485 (the 2023 low).

InstaForex analytical reviews will make you fully aware of market trends! Being an InstaForex client, you are provided with a large number of free services for efficient trading.