Permanecer

Permanecer

Condições de Negociações

Ferramentas

December 16 show that since mid-November, the aggregate position for the US dollar against major world currencies has been steadily worsening. This reflects the market's reevaluation of the outlook for both the Fed's rate movements and the US economy as a whole. There's no reason to believe this trend will change in the near future; all the negative factors that have pressured the dollar in recent weeks continue to exert their influence.

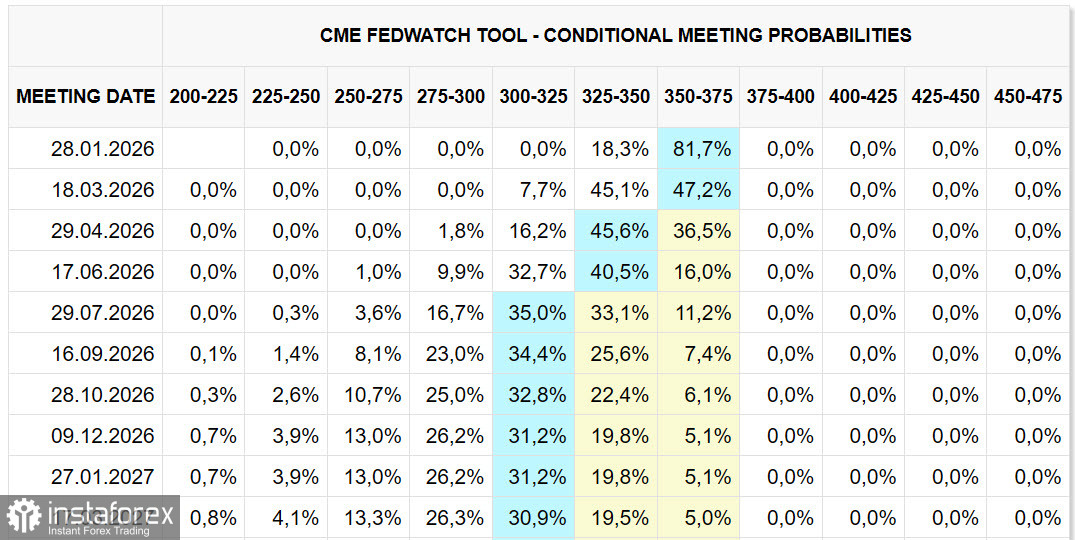

The Fed's interest rate forecast implies two cuts next year—in April and July. What happens afterward remains a mystery, and even these two reductions are not guaranteed. Everything is changing rapidly; recall the forecasts for the last meeting when, at the beginning of November, the markets were convinced that the Fed would maintain the rate, but by the end of November, that opinion had completely reversed.

There are too many factors increasing uncertainty. The state of the US labor market points to a decline in economic activity, while GDP growth for Q3, on the contrary, appears quite positive. ISM reports tend to show deterioration, yet the stock market remains near historical highs, primarily supported by hopes of growth in the technology sector. However, if doubts arise about AI prospects, the market could simply crash. A similar scenario unfolded in the early 2000s when technology sector companies were rapidly growing.

The US dollar appears stable, and its status as the world's primary currency remains unchallenged, but the record growth in gold (as well as silver and platinum) indicates that the financial system is experiencing a severe crisis of trust, while the dynamics of oil, copper, and aluminum—i.e., the commodities forming the basis of the real economy—look far worse.

The Fed's independence is at risk, and many changes could occur in the coming weeks, especially regarding the Fed's composition favoring rate-cutting policies. Trump intends to go all the way here, but inflation has yet to feel the pressure from new tariffs, and the situation could change at any moment.

President Trump himself adheres to a weak dollar policy, having repeatedly stated his preference for lowering the exchange rates of the yen and yuan, which he believes could improve the US trade balance.

Here's a brief forecast for the dynamics of major currencies in the first weeks of 2026:

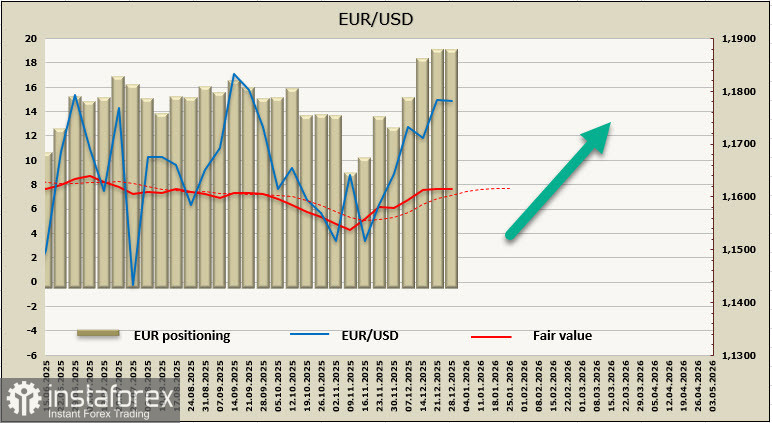

EUR/USD

The ECB has concluded its rate-cutting cycle, and the latest meeting has revised GDP and core inflation forecasts upward. This general monetary policy approach suggests a resilient euro, which acts as a bullish factor for the euro in light of the Fed's rate forecasts.

Positioning remains bullish; in the second half of November, a trend towards increasing long speculative positions in euros emerged, and the latest CFTC reports indicate that this trend is strengthening.

The probability of a pullback to the support zone of 1.1690/1730 remains, but such a pullback can only have technical reasons as there are no fundamental grounds for a deep decline in EUR/USD. We expect movement towards 1.1919; additional adjustments could come from the publication of new data, with significant upcoming events including the ISM report in the US manufacturing sector on January 5, the Eurozone PMI on January 6, and Eurozone inflation and ISM in the services sector on January 7. Before the publication of this data, we anticipate low trading activity with a slow upward trend.

GBP/USD

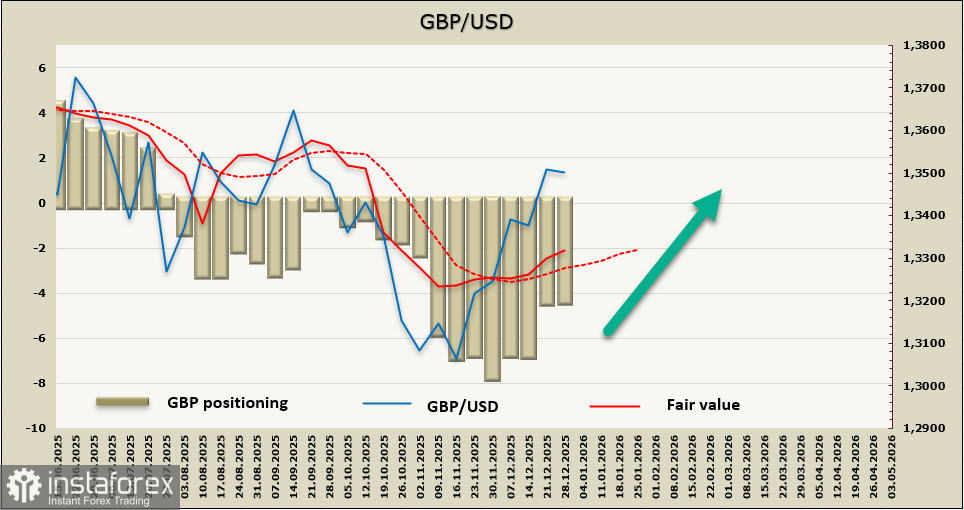

The pound appears somewhat weaker than the euro, but its dynamics are likely to be similar. Although the Bank of England cut rates at the last meeting, the vote for a cut was minimal, and now markets expect only one reduction next year, which will keep the rate at a relatively high level of 3.5%. The primary factor here is the threat of persistently high inflation in the UK, which will remain above US levels for a long time, clearly restraining the Bank of England and providing support for the pound.

The short speculative position in the pound has been actively reducing in recent weeks, and we expect this trend to continue. The pound will seek resistance at 1.3620/40; rising would increase the likelihood of a technical correction, but it is unlikely to be deep, as support at 1.3370/90 appears robust. The first week of the new year will have little significant statistics for the pound, so the overall trading dynamic will largely be influenced by news from the US.

NZD/USD

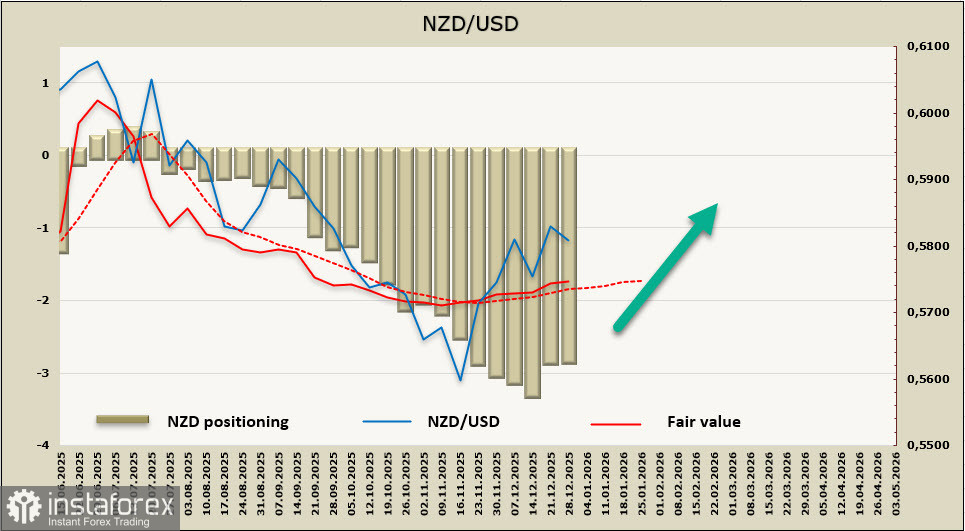

New Zealand's economy has gone through a serious test, facing high inflation alongside negative GDP dynamics. The third quarter proved positive, and growth is also expected in the fourth quarter, with the RBNZ's policy looking quite predictable.

In November, the RBNZ cut rates to 2.25%, but inflation dynamics in recent months clearly favor a return to growth. As the economy recovers at the current rate, further cuts are unlikely, and furthermore, the RBNZ is expected to start raising rates in the second half of the upcoming year, making three increases by May 2027. Accordingly, the policies of the Fed and RBNZ will be oppositely directed, with the kiwi gaining an advantage due to changes in yield spreads.

Positioning for the kiwi remains bearish, and currently, there are almost no signs of a reversal. However, there are good grounds to assume that the next couple of CFTC reports will favor increased demand for NZD.

The NZD/USD pair has strengthened significantly since November 20, and we expect this growth to continue. A technical correction seems unlikely, and support at 0.5731 is unlikely to be reached, while an attempt to reach the technical level of 0.5910 appears more realistic. The next news from New Zealand that could support the kiwi is expected only on January 12 (the NZIER report for Q4, which may adjust GDP forecasts) and the inflation index for Q4 on January 20. If it shows sustained inflation levels, the kiwi may receive an additional bullish impulse. For now, we assume that trading in the first week of the year will be inactive with a slight upward shift.

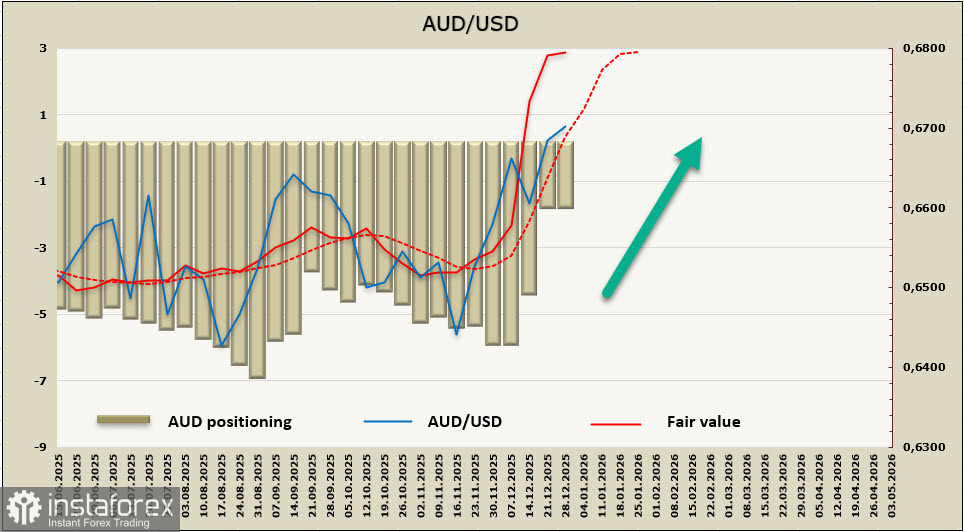

AUD/USD

Unlike other major currencies, the Aussie may start the year quite actively. On January 1, the PMI report for the manufacturing sector will be published, followed on January 6 by the PMI report for the services sector and on January 7 by the monthly report on consumer inflation for November. Given that inflation has already risen from a low of 1.9% in June to 3.8% in October, the new report will be very significant for the further dynamics of the Aussie, as it will influence forecasts for the RBA's rates. The market currently assumes that the rate-cutting cycle has ended, and if November's inflation shows at least stability, the market will likely anticipate an earlier start to the rate-hiking cycle, which will automatically support the Australian dollar.

The last two CFTC reports showed a sharp increase in demand for AUD, with the calculated price rapidly rising, which is a clear sign of increasing bullish momentum.

The AUD/USD pair has reached a high not seen since October 2024, increasing the likelihood of a technical correction. We expect a decline below support at 0.6670/80 to be unlikely and to occur only if large players take profits ahead of the new year. In any case, a correction is not expected to be prolonged, as fundamental factors favor continued growth.

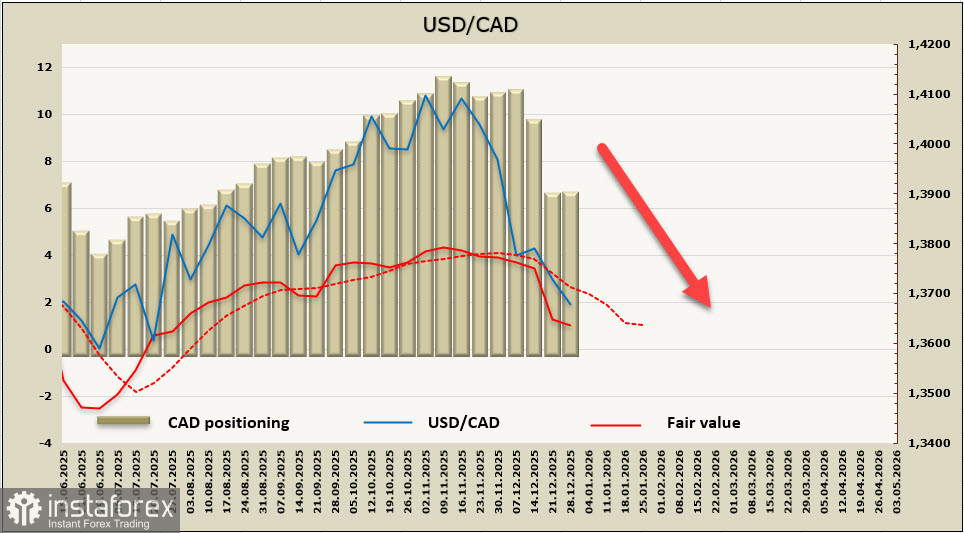

USD/CAD

Forecasts for the Bank of Canada's rate are currently unstable. The Bank views the current rate of 2.25% as close to neutral, but additional confirmations are needed for this opinion to solidify. The market remains cautious regarding the assumption that the Bank of Canada has ended its rate-cutting cycle, as it awaits the labor market report for December (due on January 9) and the inflation report (January 19). Currently, the Canadian dollar appears more convincing than its larger counterpart, but the situation is complicated by the fact that the Canadian economy depends more on the U.S. situation, given the deep mutual integration.

The calculated price suggests further declines in USD/CAD; the last two CFTC reports indicated increased demand for CAD, but additional confirmation is needed.

The rapid decline of USD/CAD in recent weeks raises the likelihood of a technical correction. We believe that the pair will not rise above 0.3800/20. For further declines, there are no particular reasons at present; new data are required. However, in the long term, we believe that an attempt to reach support at 0.3536 is more likely than a reversal upward.

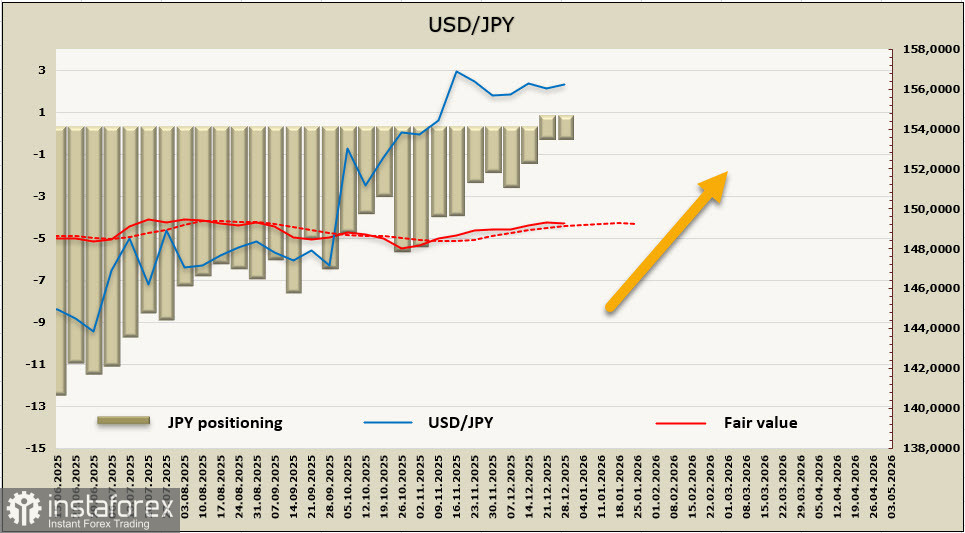

USD/JPY

The yen remains the most enigmatic currency. Markets reacted with strengthening yen after the Bank of Japan, after months of deliberation, raised rates, but the movement quickly halted. The cause of this was a new wave of uncertainty following the release of inflation data from the Tokyo region, which showed a sharp slowdown in price growth from 2.7% y/y to 2.0%, with the core index excluding food slowing from 2.8% to 2.3%.

If this trend is confirmed at the national level, talks of another rate hike could be forgotten for a long time. The Bank of Japan will take time to analyze economic growth indicators, wait for the results of wage negotiations between unions and the government, and comment on the state of affairs in vague terms. Since the inflation report will not be published until January 22, there is unlikely to be a clear factor that could give the yen momentum before then.

The strong bullish bias for the yen has been completely eliminated, and speculative positioning is currently neutral. We see no reason to expect strong movements in either direction, as fundamental factors do not present a clear picture. From a technical perspective, a decline seems more likely, especially given the growing dissatisfaction from the US regarding a too-weak yen, but Japan cannot afford a stronger yen amid rising government debt interest payments and a clear economic crisis; thus, we have to refrain from providing a forecast for the yen for now.

InstaForex analytical reviews will make you fully aware of market trends! Being an InstaForex client, you are provided with a large number of free services for efficient trading.