Maradok

Maradok

Kereskedési feltételek

Products

Eszkozok

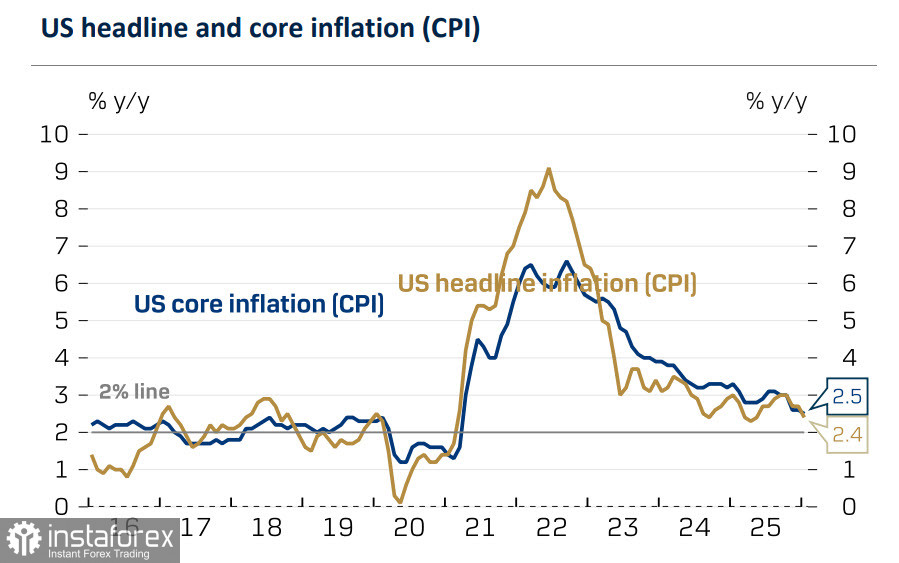

The US January inflation report came in slightly better than the market had forecast: consumer prices rose 0.2% month-on-month versus a 0.3% estimate, and annual inflation slowed from 2.7% to 2.4%, the weakest reading since last spring. Core inflation eased only modestly, from 2.6% year-on-year to 2.5%, but that is still the lowest level since March 2021.

With inflation slowing, market pricing now implies at least two Federal Reserve rate cuts this year, in March and June, and Treasury yields have fallen to their lowest levels in a year.

It is becoming increasingly clear that the market's initial upbeat reaction to January's employment report was misplaced. The anticipated inflationary impulse from new tariffs has not materialized, and the balance of risks has shifted toward a third Fed rate move this year, which intensifies pressure on the dollar.

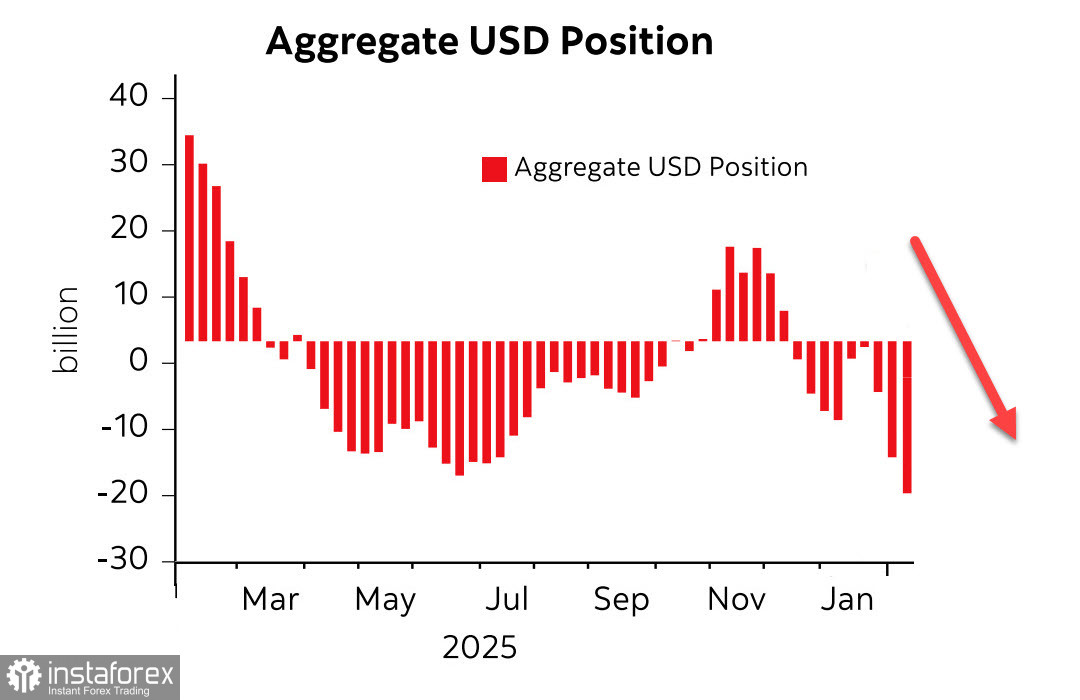

The CFTC report published on Friday showed that the dollar sell-off trend continues. Net short positioning against major global currencies rose by $2.5 billion over the reporting week to –$19.9 billion, with the largest increase again recorded against the euro, where the net long position climbed to $26.8 billion.

Over the past year, the dollar index has lost more than 9%, which makes imports more expensive for US consumers but benefits exporters by making them more competitive — an outcome aligned with the Trump administration's doctrine. In Q4 2025, the S&P 500 companies with more than 50% of revenue generated abroad saw profits rise by 19%; on average, all index constituents reported profits up about 18% and revenue up nearly 12%. In other words, US corporates are benefiting from a weaker dollar.

At the same time, investor confidence in the United States is weakening. Fund managers are cutting US exposures, and some report full sales of Treasuries. If foreign investors seek to reduce their US holdings, they must sell assets, but that process cannot be rapid while the United States runs a current account deficit that is trending higher; selling to US buyers is constrained by limited domestic liquidity.

The only practical mechanism for that portfolio rebalancing is a relative repricing of US assets — namely, a weaker dollar. A lower dollar, therefore, facilitates the shift in global asset allocations.

The Congressional Budget Office's panel expects the federal budget deficit in fiscal 2026 to reach $1.9 trillion, or 5.8% of GDP, largely driven by rising net interest costs.

In short, a weaker dollar both reduces confidence in the US assets and increases corporate revenues. Protective tariffs further boost US companies' competitive position. Those twin processes reinforce administration priorities.

Taken together, while the US current account deficit remains large and rising, the dollar is unlikely to regain strength in the near term.

Risks hinge on the interplay between US growth momentum and aggregate consumer demand. Until Friday's releases of the revised Q4 GDP figures and the personal consumption expenditures (PCE) price index, forecasts are unlikely to change materially; thereafter, the outlook will turn on incoming data. There are too many contradictory indicators: some point to solid growth, others to the risk of recession. Some show robust consumer demand, others a slowdown. For now, the most likely scenario for the coming week is further dollar weakness.

InstaForex analytical reviews will make you fully aware of market trends! Being an InstaForex client, you are provided with a large number of free services for efficient trading.