Permanecer

Permanecer

Condições de Negociações

Ferramentas

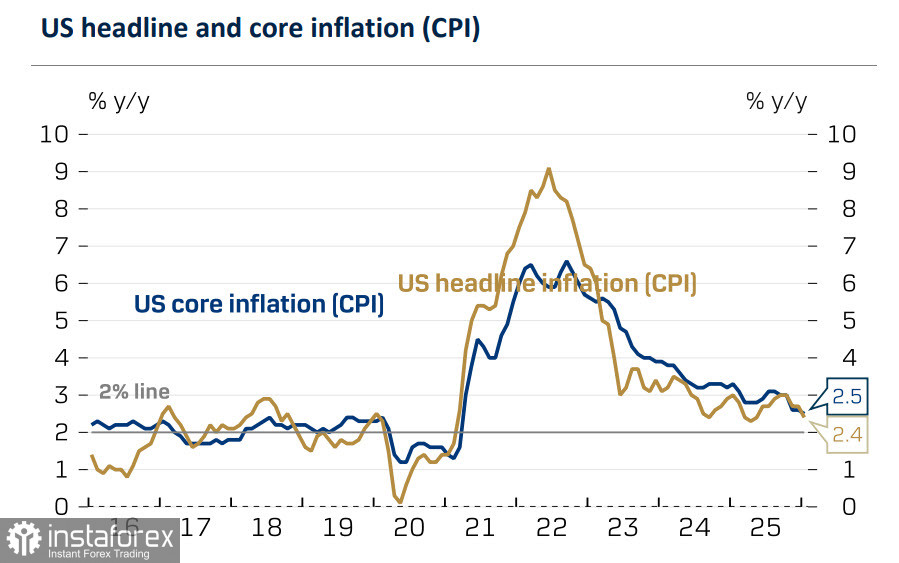

O relatório de inflação dos EUA em janeiro ficou ligeiramente melhor do que o mercado havia previsto: os preços ao consumidor subiram 0,2% em relação ao mês anterior, contra uma estimativa de 0,3%, e a inflação anual desacelerou de 2,7% para 2,4%, o menor índice desde a primavera passada. A inflação básica diminuiu apenas modestamente, de 2,6% em relação ao ano anterior para 2,5%, mas ainda assim é o nível mais baixo desde março de 2021.

Com a desaceleração da inflação, a precificação do mercado passou a indicar pelo menos dois cortes de juros pelo Federal Reserve ainda este ano, em março e junho. Em resposta, os rendimentos dos Treasuries — títulos públicos emitidos pelos EUA — recuaram para os níveis mais baixos em um ano.

Fica cada vez mais evidente que a reação inicial otimista do mercado ao relatório de emprego de janeiro foi equivocada. O impulso inflacionário esperado a partir das novas tarifas não se materializou, e o balanço de riscos passou a favorecer um terceiro movimento do Fed ao longo do ano, o que aumenta a pressão sobre o dólar.

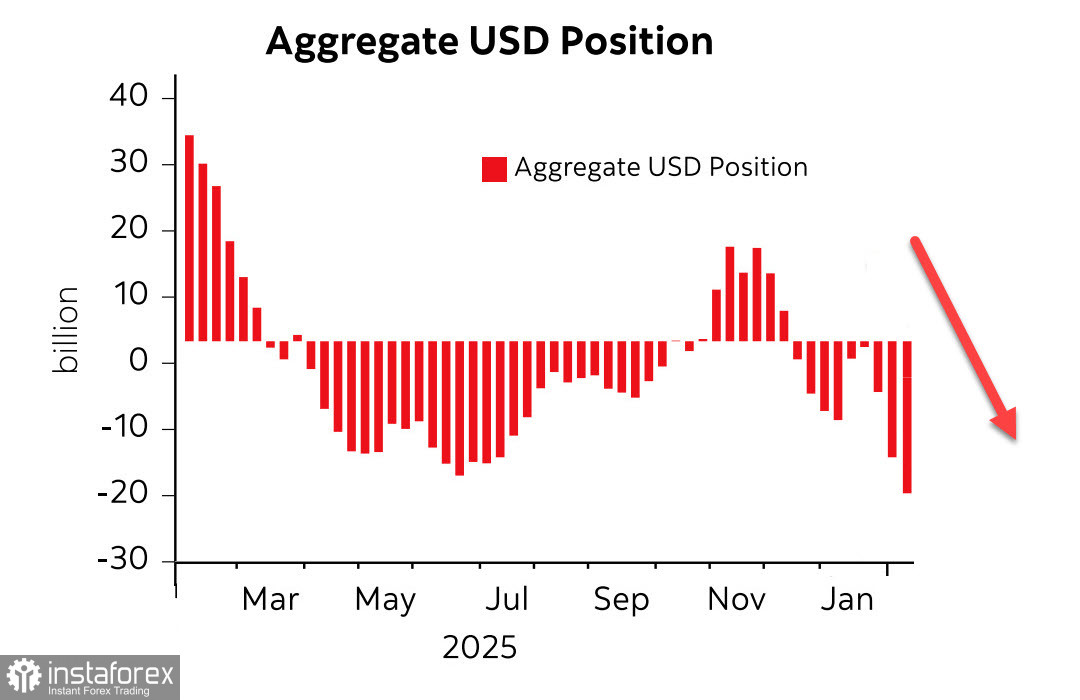

O relatório da CFTC, divulgado na sexta-feira, mostrou que a tendência de venda da moeda americana permanece intacta. A posição líquida vendida contra as principais moedas globais aumentou em US$ 2,5 bilhões na semana de referência, alcançando –US$ 19,9 bilhões. O maior avanço voltou a ocorrer frente ao euro, cuja posição líquida comprada subiu para US$ 26,8 bilhões.

No último ano, o índice do dólar recuou mais de 9%, o que encarece as importações para os consumidores americanos, mas beneficia os exportadores ao torná-los mais competitivos — um resultado alinhado à doutrina da administração Trump. No quarto trimestre de 2025, as empresas do S&P 500 com mais de 50% da receita gerada no exterior registraram crescimento de lucros de 19%; em média, todos os componentes do índice reportaram lucros cerca de 18% maiores e receitas quase 12% mais elevadas. Em outras palavras, as empresas americanas estão se beneficiando de um dólar mais fraco.

Ao mesmo tempo, a confiança dos investidores nos Estados Unidos vem enfraquecendo. Gestores de fundos estão reduzindo a exposição ao mercado americano, e alguns relatam vendas integrais de Treasuries. Se investidores estrangeiros buscam diminuir suas participações nos EUA, precisam vender ativos — mas esse processo não pode ocorrer de forma rápida enquanto o país mantém um déficit em conta corrente em trajetória de alta; além disso, a capacidade de absorção por compradores domésticos é limitada pela liquidez interna reduzida.

O único mecanismo prático para esse reequilíbrio de carteiras é a reprecificação relativa dos ativos americanos — ou seja, um dólar mais fraco. Um dólar depreciado, portanto, facilita a realocação global de ativos.

O painel do Congressional Budget Office projeta que o déficit orçamentário federal no exercício fiscal de 2026 alcance US$ 1,9 trilhão, equivalente a 5,8% do PIB, impulsionado em grande parte pelo aumento dos custos líquidos com juros.

Em síntese, um dólar mais fraco reduz a confiança nos ativos dos EUA ao mesmo tempo em que eleva as receitas corporativas. Tarifas protecionistas reforçam ainda mais a posição competitiva das empresas americanas. Esses dois processos caminham em consonância com as prioridades da atual administração.

Diante desse conjunto de fatores, enquanto o déficit em conta corrente dos Estados Unidos permanecer elevado e em expansão, é pouco provável que o dólar recupere força no curto prazo.

Os riscos dependem da interação entre o ritmo de crescimento da economia americana e a demanda agregada dos consumidores. Até a divulgação, na sexta-feira, dos números revisados do PIB do quarto trimestre e do índice de preços dos gastos com consumo pessoal (PCE), é improvável que as projeções sofram mudanças relevantes; a partir daí, as perspectivas passarão a depender dos dados que forem divulgados.

Há muitos indicadores contraditórios: alguns sinalizam crescimento sólido, enquanto outros apontam para risco de recessão. Alguns mostram uma demanda do consumidor ainda robusta; outros indicam desaceleração. Por ora, o cenário mais provável para a próxima semana continua sendo uma maior fraqueza do dólar.

InstaForex analytical reviews will make you fully aware of market trends! Being an InstaForex client, you are provided with a large number of free services for efficient trading.