Zůstat

Zůstat

Obchodní podmínky

Nástroje

See also: InstaForex trading indicators for GBP/AUD

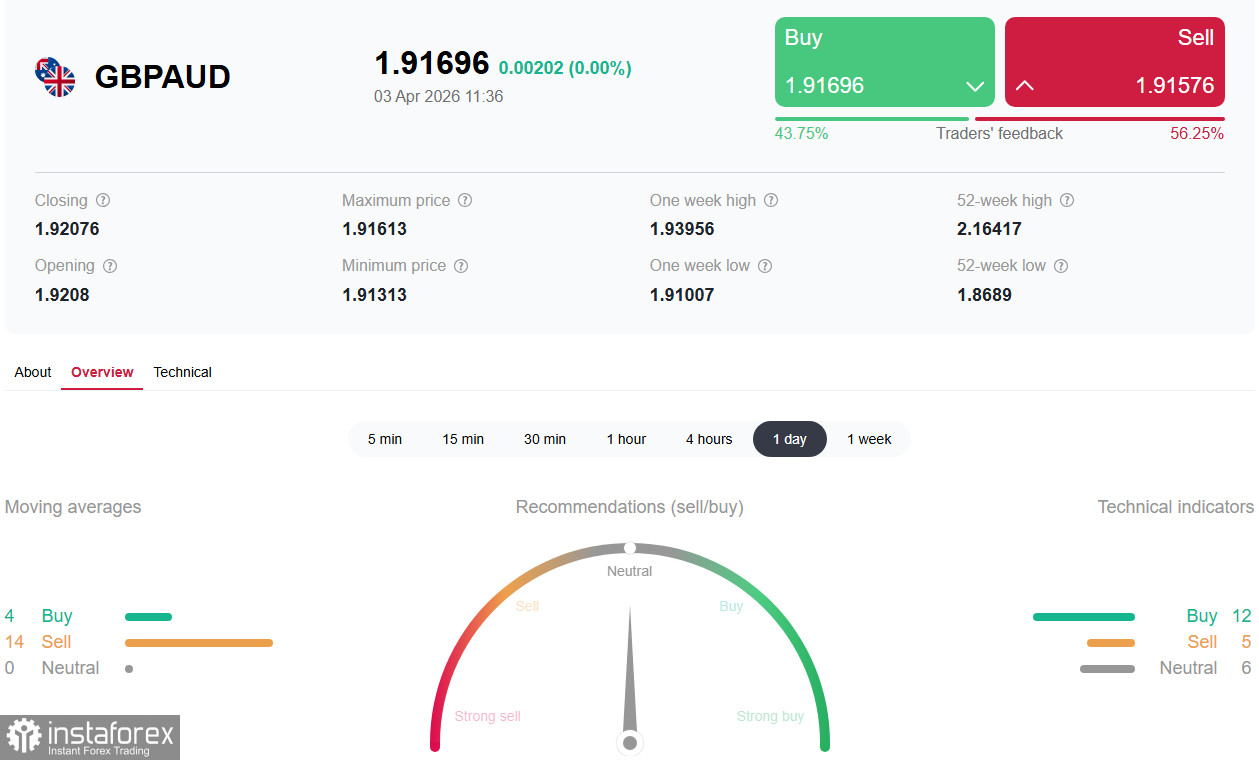

The GBP/AUD pair ends the first week of April in a state of acute uncertainty, reflecting a complex interplay of monetary expectations and geopolitical risks. While the Bank of England remains cautious, warning about overstated rate hike expectations, the Reserve Bank of Australia faces rising stagflation risks, and markets price in up to a 55% chance of a rate hike at the May meeting. Trading activity remains subdued because of Good Friday observance, and attention is focused on the upcoming US employment data.

Current situation: NFP watch and monetary policy divergence

On Friday, April 3, many trading venues are closed for Good Friday, leading to lower liquidity and elevated volatility at the Monday open. Traders are cautious ahead of the key US March employment report (Nonfarm Payrolls), due at 12:30 GMT.

At its March 19 meeting, the Bank of England left the policy rate at 3.75% but revised up inflation forecasts from 3.0% to 3.5%. At the same time, inflation expectations among UK businesses rose: most respondents now expect 12-month inflation of 3.7%, not 3.4% as previously forecast, reaching last October's high.

However, in media interviews, BOE Governor Andrew Bailey warned that investors should not price in imminent tightening and that the next decision will require careful consideration of the full set of risks. Based on these remarks, some economists reduced their expectations for the number of rate increases this year from two to one.

In Australia, the situation is different. Higher energy prices related to the Middle East conflict are pushing inflation up and strengthening expectations of further RBA rate hikes amid growing stagflationary risks. As of April 1, ASX futures on the 30-day interbank rate for May 2026 imply a 55% probability of a rate increase to 4.35% at the next RBA meeting.

Economists, meanwhile, forecast that the RBA will deliver three more rate hikes in 2026, taking the cash rate to 4.85% — a level not seen since November 2008.

Australia's external trade data, which were positive, support the view of tighter RBA policy: the trade surplus widened to AUD 5.69 billion, more than double the January reading. Exports rose 4.9% month on month, helped by an almost 30% jump in gold shipments, while imports fell 3.2%.

Exports of key commodities such as iron ore, coal, and LNG remained weak, which points to insufficient underlying demand.

It should also be noted that the most recent Australian macro data do not yet reflect the impact of the Middle East conflict, and potential effects are expected to appear in March reporting.

China, Australia's key trading partner, released a services PMI that fell to 52.1 in March from 56.7 in February, below expectations. AUD reacted fairly calmly to these figures.

Today, as noted above, the March US Nonfarm Payrolls report is due at 12:30 GMT. Market consensus expects 60,000 new jobs after a disappointing -92,000 in February, with the unemployment rate forecast to remain at 4.4%. However, some economists see upside risk to a dovish outcome and expect a softer print of around 30,000.

Weak data could weigh on the dollar and support both majors (GBP and AUD). It is important to note that because of Good Friday, the immediate market reaction may be muted and volumes low, with a delayed response at the Monday open.

Outlook: two scenarios

Scenario A (the main one): continued pressure, AUD rises

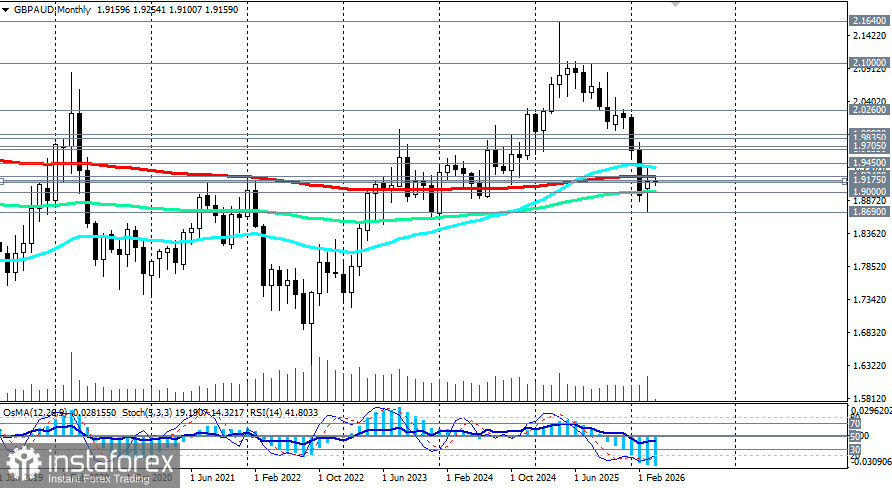

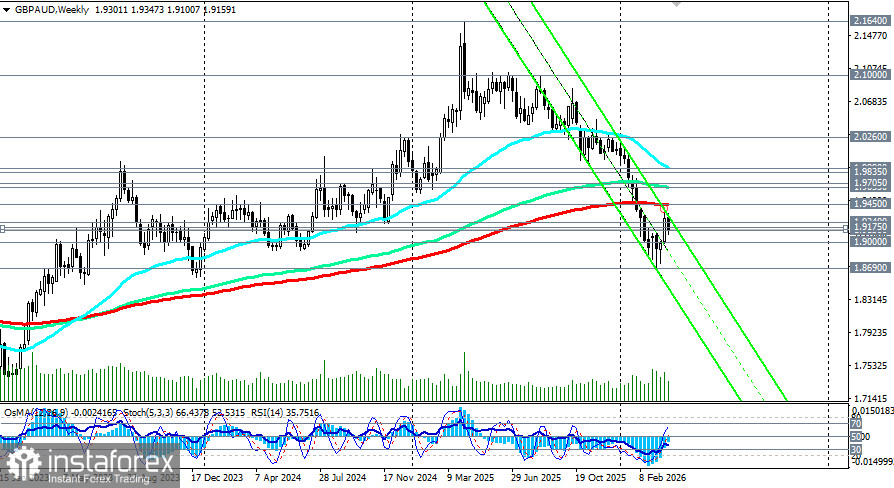

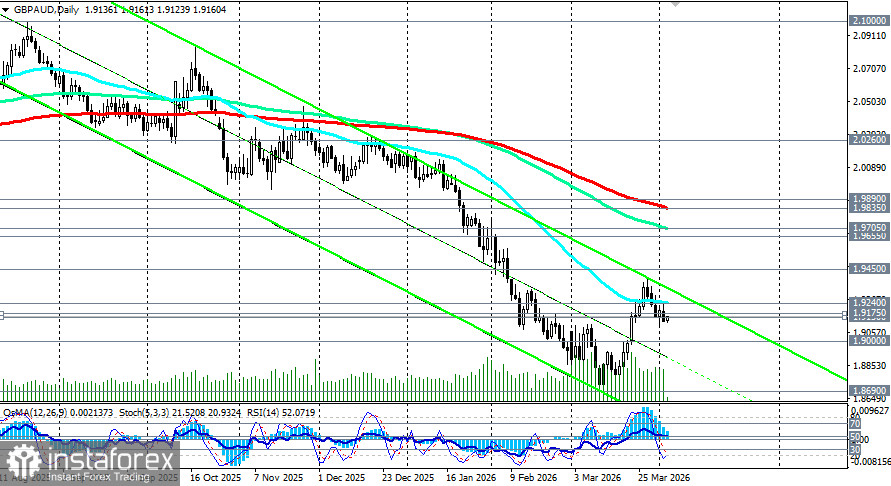

The likeliest scenario in the coming weeks is continued pressure on GBP/AUD toward 1.9000 (EMA144 on the monthly chart)–1.8860 (February lows). Hawkish RBA expectations (55% odds for a May hike) and Australia's stagflation risks may, paradoxically, support AUD as higher rates attract capital.

Triggers for this scenario:

- sustained high oil prices

- confirmation of hawkish signals from the RBA

- a cautious stance from the Bank of England

Scenario B (bearish for AUD): AUD drops

This would materialize if:

- oil prices fall below $90 amid de-escalation

- signs of a slowdown in Australia's economy emerge (weak iron ore and coal exports)

- the Bank of England delivers hawkish signals (contrary to Bailey's warnings)

Targets: a return to 1.9240 (EMA50 on the daily chart)–1.9450 (EMA200 on the weekly chart).

Conclusion

GBP/AUD is at the epicenter of a fundamental divergence. The Bank of England remains cautious and warns that rate hike expectations are overstated. The Reserve Bank of Australia, conversely, faces rising stagflation risks, and markets price in up to a 55% probability of a May rate hike.

The key zone 1.9000–1.9240 will be the arena of the decisive battle in the coming days. Holding above it will keep chances for a recovery to 1.9400–1.9450, but a break below will open the road to 1.8700–1.8500.

Under any scenario, volatility will remain high. Investors should closely monitor today's US employment data (NFP), developments around the Strait of Hormuz, and, importantly, rhetoric from RBA and BOE officials ahead of their May meetings. As Governor Bailey noted, the next decision will require careful attention to the full set of risks. Success will favor those who can weigh the balance between hawkish RBA expectations and the BOE's warnings amid ongoing geopolitical uncertainty.

Díky analytickým přehledům společnosti InstaForex získáte plné povědomi o tržních trendech! Jako zákazníkovi společnosti InstaForex je Vám k dispozici velký počet bezplatných služeb umožňujících efektivní obchodování.