Ważne do 15:00 2026-07-12 UTC--4

Informacje te są częścią komunikacji marketingowej i są przeznaczone dla klientów detalicznych i profesjonalnych. Informacje te nie zawierają i nie powinny być interpretowane jako informacje zawierające porady inwestycyjne lub rekomendacje dotyczące inwestycji, a także oferty lub zaproszenia do udziału w dowolnej transakcji, lub strategii dotyczącej instrumentów finansowych. Wcześniejsze zyski nie stanowią gwarancji przyszłych dochodów. Instant Trading EU Ltd nie udziela żadnych gwarancji i nie ponosi żadnej odpowiedzialności za dokładność lub kompletność dostarczonych informacji, a także za jakiekolwiek straty wynikające z inwestycji opartych na analizie, prognozie lub innych informacjach dostarczonych przez pracownika Firmy, lub w jakikolwiek inny sposób. Pełne oświadczenie o wyłączeniu odpowiedzialności jest dostępne tutaj.

Following the June European Central Bank meeting, during which the central bank raised rates by 25 basis points and reaffirmed its commitment to fighting inflation, the market was confident that the tightening cycle would continue. However, over the past three weeks, the central bank's rhetoric has softened: current market forecasts suggest equal probabilities for both a rate hike and a pause. Regarding the September decision, the situation remains more "hawkish": according to Danske Bank, the probability of a rate hike is about 60%.

Arguments for Maintaining the Rate:

- Slowing Inflation: June figures were below expectations (except in the energy sector), and oil prices have fallen significantly.

- Decreasing Price Pressure: Expectations for producer prices in June fell, and the services sector returned to February levels, while the producer prices index (PMI) approached pre-war values.

- Weak Economic Growth: Macroeconomic indicators for the Eurozone have underperformed against forecasts.

- Absence of Secondary Effects: There is no significant pressure on inflation from wage growth or inflation expectations.

- Balanced Rhetoric: Recent statements from ECB officials have become more measured.

Arguments for Raising the Rate:

- Tightened Stance of the Regulator: Despite the balance, the ECB's Governing Council remains committed to combating inflation.

- Economic Resilience: The Eurozone economy has shown high adaptability to external shocks, including the energy crisis and global changes in trade policy.

- Energy Factor: Prices for petroleum products and gas remain above pre-war levels, despite falling spot oil prices.

- High Inflation Expectations: In May, inflation expectations for the 1- and 3-year horizons remained at 3.5%.

- Low Real Rate: Due to high inflation expectations, the real interest rate has increased only marginally, necessitating further policy tightening.

Forecast for the EUR/USD Pair:

Markets are pricing in one rate hike each from both the Federal Reserve and the ECB by the end of the year. In this scenario, the rate differential remains stable, and the EUR/USD exchange rate will primarily be determined by incoming macro data. Under current conditions, the euro appears vulnerable: structural issues in both economies could provoke crisis phenomena, in which the U.S. dollar traditionally benefits as the primary safe-haven currency.

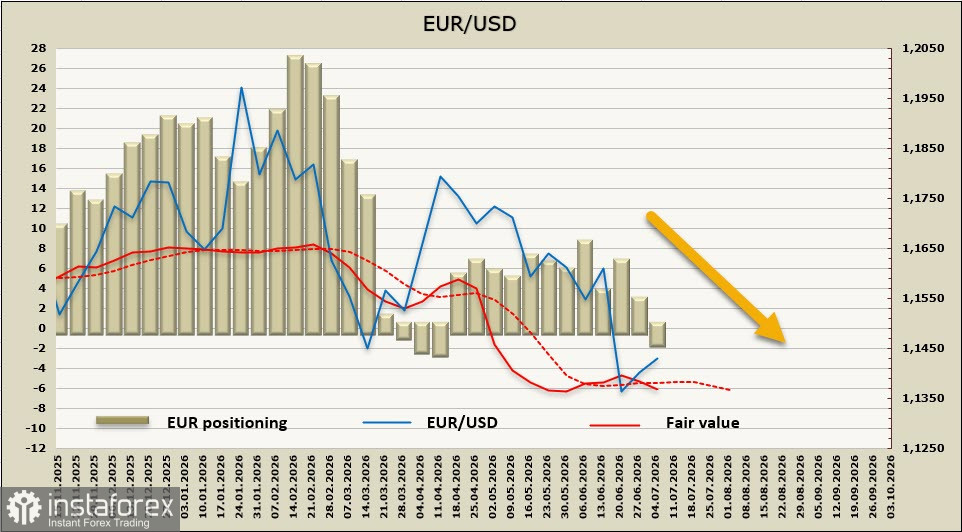

Speculative positioning in the euro is once again neutral, with net long positions decreasing by $4.1 billion over the week, nearly returning to zero, and the estimated price moving down from the long-term average.

A week ago, we anticipated further declines in EUR/USD, and this forecast remains relevant despite the euro's slight correction following last week's drop. We expect a retest of the technical level at 1.1353 and a move toward support at 1.1128. The corrective impulse is nearly exhausted, and the chances for growth toward the nearest resistance at 1.1500 are quite slim.

Otwórz konto handlowe w InstaForex

Dzięki analizom InstaForex zawsze będziesz na bieżące z trendami rynkowymi! Zarejestruj się w InstaForex i uzyskaj dostęp do jeszcze większej liczby bezpłatnych usług dla zyskownego handlu.

Anuluj

Anuluj