Zůstat

Zůstat

Obchodní podmínky

Nástroje

*) see also: InstaForex trading indicators for S&P 500 (SPX)

As the Sultanate of Oman Foreign Minister Badr bin Hamad bin Hamad al-Busaidi said, the recent discussions in Switzerland between the United States and the Islamic Republic of Iran on the nuclear program showed significant progress.

Participants now plan to hold additional internal consultations before resuming discussions of key issues at the next round of talks, scheduled for Vienna next week.

At the same time, experts believe the parties have not yet achieved real progress or consensus. Despite encouraging signals, the minister's statement so far has had little impact on risk-asset markets, where sentiment remains unstable.

Nevertheless, leading US equity indices, in particular the S&P 500, may close the week with a small but positive gain.

Geopolitical tension around Iran persists, but talks in Geneva achieved "significant progress," which reduces the risk of escalation.

Current situation: macroeconomic support

Equity indices also benefit from positive macro data out of the United States released overnight. The Labor Department's weekly report showed a small rise in initial jobless claims from 208k to 212k, below the 215k forecast. The total number of people receiving benefits fell to 1.833 million (from 1.864 million), and the four-week moving average adjusted to 220.25k.

Another positive signal came from the Mortgage Bankers Association (MBA): the average 30-year mortgage rate fell to 6.09% from 6.17%, which boosted mortgage applications by 0.4% after a 2.8% rise the week before. Stability in the labor and housing markets strengthens the Fed's case to hold policy unchanged at the March meeting.

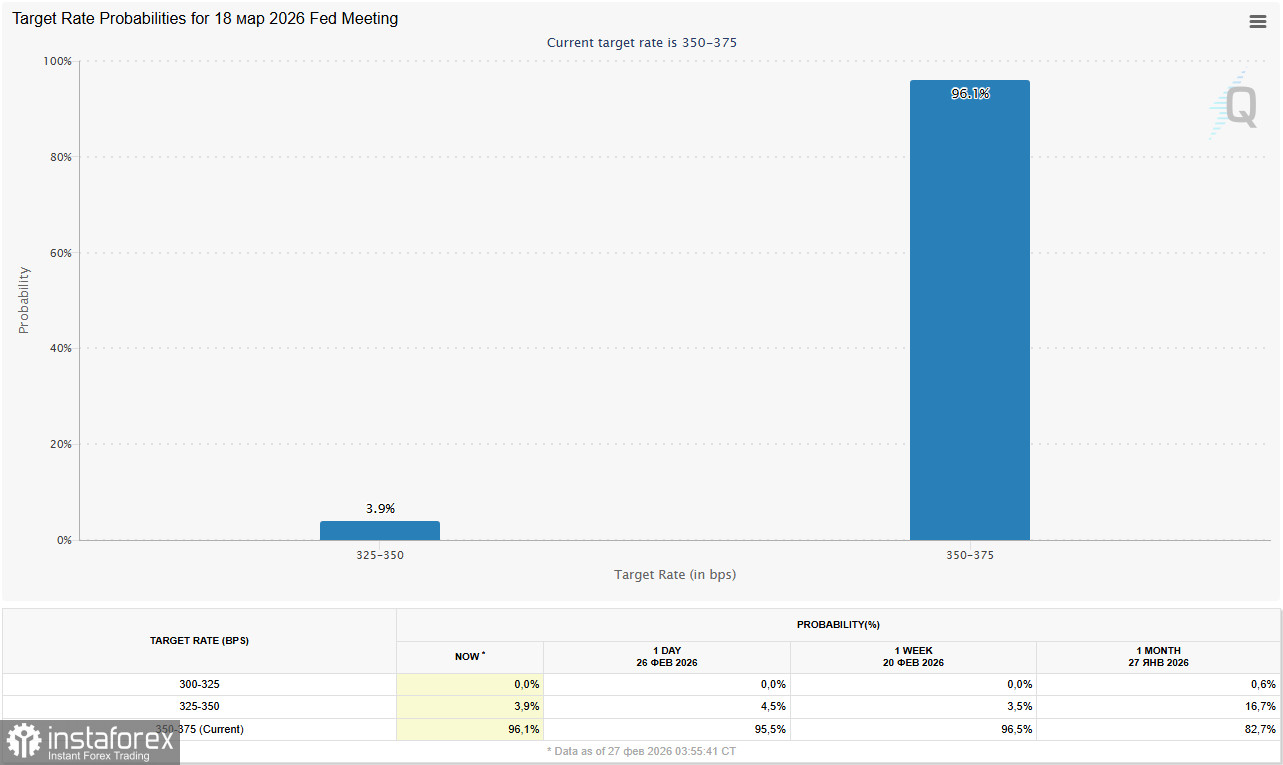

According to the CME FedWatch Tool, the market today assigns a 96.0% probability that the policy rate will remain in the 3.50%–3.75% range at the 18 March meeting. Traders do not expect changes to monetary policy conditions until mid-summer, when Jerome Powell's term as Fed chair ends. Powell himself will retain a two-year mandate as a member of the Board of Governors, which could materially affect the balance of power in future votes.

CME FedWatch data show the probability of a rate cut in June has fallen to 40%; July is now viewed as a more likely timing for the first cut (65%), as noted in yesterday's review, "USD/CHF: geopolitics and prospects."

Corporate sector: tech giants set tone

NVIDIA Corp. management reported revenue of $68.1 billion, markedly higher than $57.0 billion in the prior quarter and $39.33 billion a year earlier. Earnings per share were $1.62, beating $1.30 and $0.89, respectively. Despite strong results, Nvidia shares fell 5.5% after the report as investors remain wary about a potential AI bubble and concerned over the ability to recoup heavy investment.

Salesforce Inc. confirmed revenue of $11.2 billion (versus $10.3 billion and $9.99 billion), and EPS came in at $3.81, surpassing prior figures of $3.25 and $2.78. The company also announced a $50 billion share-repurchase program and a 5.8% dividend increase.

Top gainers in the index included Caesars Entertainment Inc. (+19.11%), Paramount Skydance Corp. (+10.04%), GoDaddy Inc. (+8.95%), and J.M. Smucker Co. (+8.82%).

Technical picture

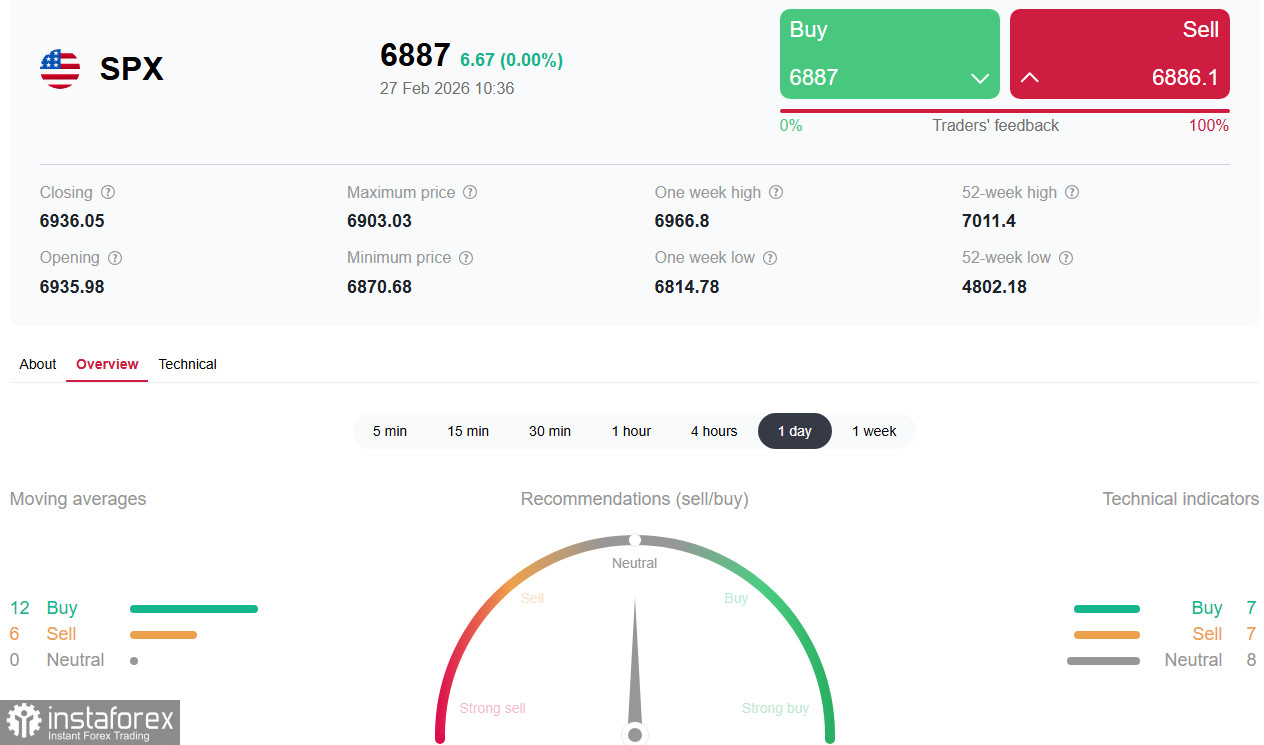

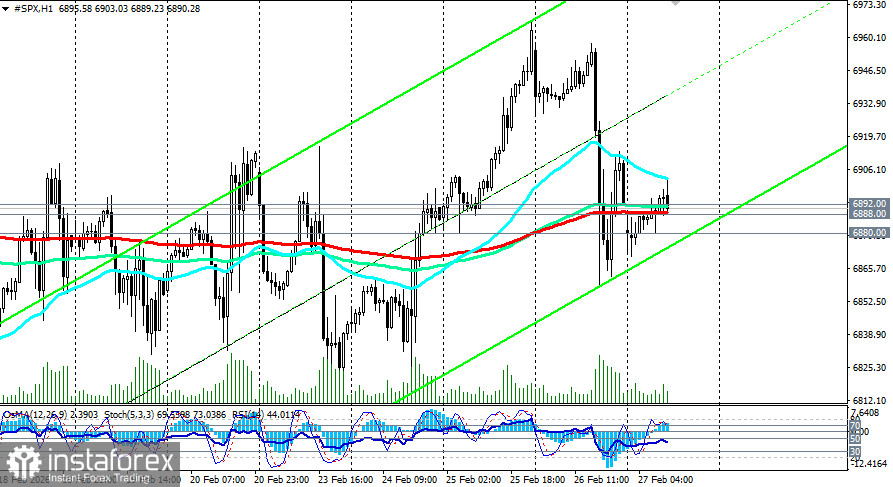

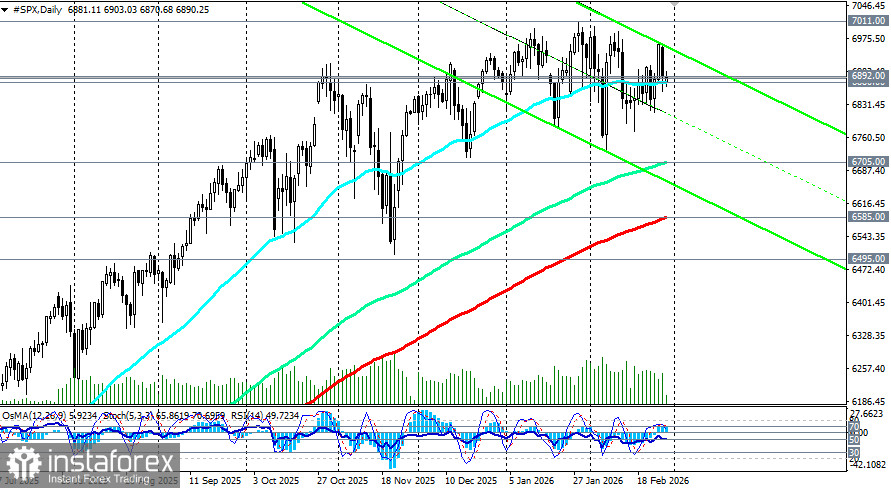

Ahead of the opening of the US trading session and at the time of this publication, the S&P 500 futures are trading around key short-term support levels at 6,888.00 (EMA200 on the 1-hour chart) and 6,892.00 (EMA200 on the 4-hour chart), while the index remains within a stable bullish regime—medium-term, long-term, and global (see more in the review "S&P500 (SPX): dynamic scenarios for 27.02.2026").

The S&P500 holds its bullish position, trading above key moving averages. Immediate resistance is near 6,970.00–7,000.00, with support in the 6,870.00–6,800.00 area. A break above 7,000.00 would open the way to test historical highs, while a breakdown of support could prompt a correction toward the 6,700.00–6,650.00 range.

Conclusion

The US equity market ends the week with moderate optimism, backed by solid macro data and impressive corporate results. However, ongoing uncertainty over Fed policy, geopolitical risks, and questions about the returns on AI investments create the potential for increased volatility in March.

Some economists warn that a 10% correction in equities could shave about 0.5 percentage points from GDP forecasts, and a 20% decline could cut nearly 1 percentage point. Nevertheless, they remain broadly constructive on the U.S. economy, forecasting 2.5% GDP growth in the fourth quarter, supported by fiscal stimulus and eventual monetary easing.

The key near-term factor will be the transition of leadership at the Fed and signals from the incoming chair about the future path of rates. Today's economic calendar includes the US PPI release at 13:30 GMT. If inflation comes in above forecasts, the dollar will be supported. If the data confirm a slowdown in price pressures, markets may more actively price in up to three rate cuts this year, which would increase pressure on the USD and support equity indices.

Díky analytickým přehledům společnosti InstaForex získáte plné povědomi o tržních trendech! Jako zákazníkovi společnosti InstaForex je Vám k dispozici velký počet bezplatných služeb umožňujících efektivní obchodování.