Anuluj

Anuluj

Warunki handlowe

Narzędzia

I have the uncomfortable feeling that the market has underestimated both the importance of the Federal Reserve decision in June and the decision of the European Central Bank. Both regulators in a probably coordinated way decided to turn the taps with cheap money soon.

In my view, global investors have underestimated the consequences of the recent Fed and ECB monetary policy decisions and here is why:

First, changing the Fed's policy should guarantee a continuation of the bear trend in the debt market. The still ridiculously low yields on US bonds will probably grow with interest rates in the Federal Reserve. In such an environment it would be strange if the dollar did not gain against the euro, yen or pound, not even mention emerging currencies.

Secondly, the Fed's will probably not go unnoticed in Europe and Asia. The ECB, the Bank of Japan, and the Bank of England can not afford to disregard the Americans and will soon be taking their first steps towards ending the unprecedented monetary expansion. We already have the first effect - the ECB announced the end (conditional, but still) of its own QE together with December 2018.

Thirdly, the more restrictive (or rather more normal) Federal Reserve policy is a disastrous news for emerging markets. If the American investors will be able to safely earn 3-4% in Treasury securities in America, they will probably withdraw the cash invested in risky assets in some kind of Poland, Thailand or Brazil. The effects of the Fed's actions have already been experienced by residents of Argentina and Turkey, where local currencies suffered a breakdown. The market participants have observed the retreat of foreign capital from the emerging markets from mid-April. Higher US rates will probably only consolidate or even strengthen this move.

Fourthly, the risk of collapse in US share prices is on the rise. This is partly because the growing profitability of Treasuries increases the profitability of the alternative to extremely overvalued shares, but also partly because some investors can compensate for losses in emerging markets by realizing profits from US shares. And with the automatic investment systems, a ready recipe for Wall Street busting. A foretaste of what may happen, we already had in February.

In conclusion, if the most important central banks have actually started a coordinated retreat from the ultra-low monetary policy, then the bull market days are numbered. The more so that the bull is no longer young: the bull market in America is already 9 years old, which is a very old age for this species. Also, indices in Europe have many years of strong growth behind them. The scale of the coming breakdown will be directly proportional to the credit excesses of the last decade, which are unprecedented in history. Central banks, restoring long-sighted normality, simultaneously prepare a powerful crisis, during which 2008 will be a nice memory. Investors should therefore be prepared for a strong sell-off of both stocks and bonds. A strong dollar will put pressure on emerging markets. It's time to fasten your seatbelt and go on defensive positions.

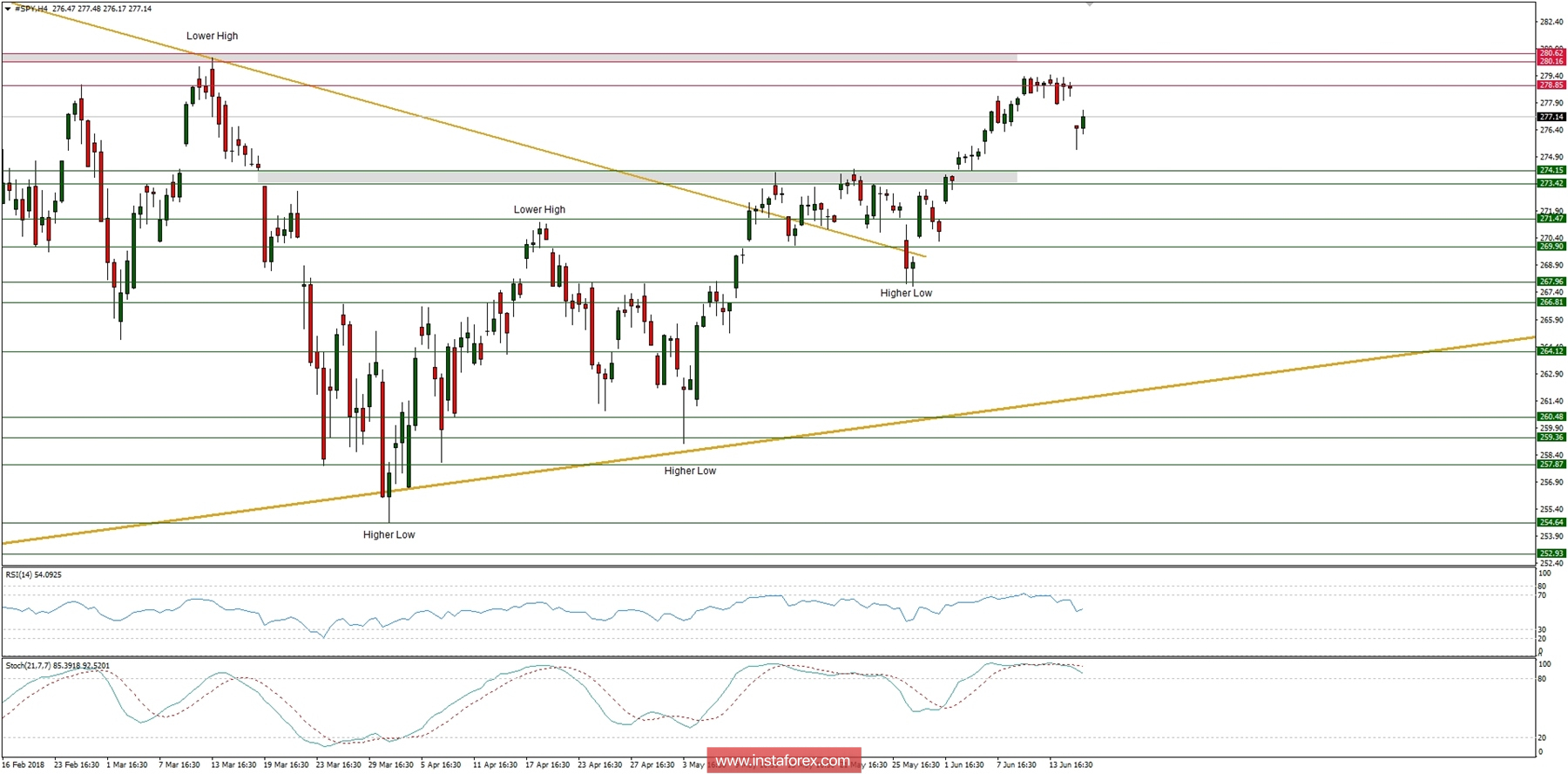

Let's now take a look at the SP500 technical picture at the H4 time frame. The market has opened gap down at the level of 275.24 and it looks like the bears want to test the recent breakout above the old resistance zone (now support) between the levels of 273.42 - 274.15. The key level to the upside is still seen at the level of 280.61, but so far the momentum is weak and the market conditions are now overbought, so this situation a corrective pull-back down is being favored.

Dzięki analizom InstaForex zawsze będziesz na bieżące z trendami rynkowymi! Zarejestruj się w InstaForex i uzyskaj dostęp do jeszcze większej liczby bezpłatnych usług dla zyskownego handlu.