Stay

Stay

Trading Conditions

Products

Tools

The USD/RUB bears were losing ground as the US stock indices slowed down their rally after the FOMC meeting in June. Besides, the increased risk of Brent falling below the psychologically important mark of $40 per barrel put more pressure on the bears. The Fed is not going to follow the example of Japan in controlling bond yields, which could potentially put an end to raising debt market rates and inspire carry trading. It has been forecasted that American oil production will rise by 20% by the end of August. This means that oil rally in May was excessive, and it is now time for a correctional decline. However, the ruble traders are not discouraged by a slight deterioration of external background and are ready to use this pullback for opening long positions on the pair.

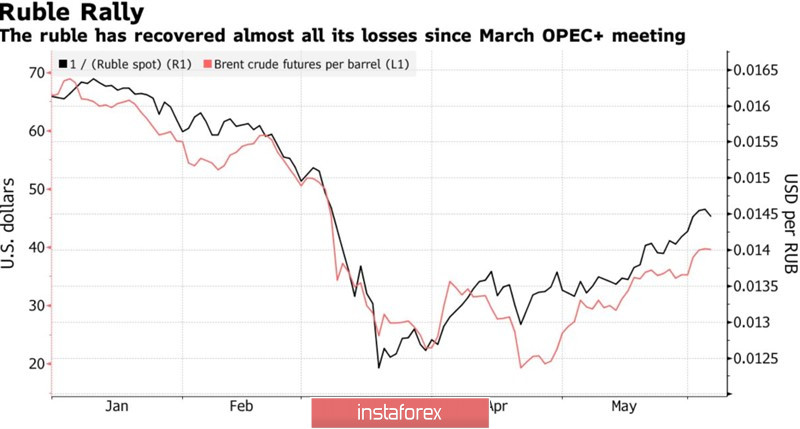

Rising oil prices and carry trading were the main supporting factors for the dollar/ruble bears in the late spring. The correlation between Brent and the Russian currency rate has increased significantly. The OPEC+ agreement on output cuts, limitation of shale oil production in the US, and recovery of global demand have pushed black gold to its highest levels since early March. At the same time, there have been speculations in the market that oil was growing too fast in response to the unprecedented rally of the US stock market. Goldman Sachs predicts a correctional decline of the North Sea grade to $35 per barrel, which is likely to lead to a pullback in the USD/RUB pair.

RUB and oil dynamics

The ruble's rise and the most rapid decrease in volatility in emerging markets since 2011 inspired traders to turn to the contracts for differences. Since the beginning of the second quarter, the efficiency of investments in Russian assets under the carry trade amounted to 21%. What is more, the intention of the Bank of Russia to continue the easing of the monetary policy sparks more interest in the ruble. Elvira Nabiullina has signaled a possible cut of the key rate by at least 1 percentage point from 5.5% to 4.5%. However, major market players believe that the regulator will go even further. Weak domestic demand and the strengthening of the national currency make it difficult to return inflation to the target of 4%. So, according to Citi, BofA Merrill Lynch, and Deutsche Bank, the key interest rate may drop to 3-4%.

The ruble, alongside other currencies of the developing countries, is supported by cheap liquidity inflows and by ultra-soft monetary policy of the world's central banks. Despite the reluctance to target yields, the Fed intends to buy $120 billion of treasuries and mortgage bonds per month under the QE program. It is also planning to keep the federal funds rate at 0-0.25%, at least until the end of 2022. As for the European Central Bank, analysts at Citi believe that the increase of the emergency asset purchase program by €600 billion is not enough to offset the EU fiscal stimulus. It is expected that the European QE program will be expanded by the year end.

As far as I see it, the pullbacks in the stock and oil markets will be short-lived. US oil producers have significantly reduced their business investment, and a return to the previous levels of shale production seems problematic. Besides, Donald Trump is most probably interested in keeping the S&P 500 up ahead of the presidential election. As a result, a rollback on the USD/RUB pair to the levels of 70.15, 70.85 and 70.1 will allow opening more short positions. In addition, moving averages and key pivot levels are seen near these marks.

USD/RUB daily chart

InstaForex analytical reviews will make you fully aware of market trends! Being an InstaForex client, you are provided with a large number of free services for efficient trading.