Stay

Stay

Trading Conditions

Products

Tools

As stated in yesterday's review, due to the lack of new drivers, including news, further strengthening of the dollar and a decrease in stock indices are likely, but so far, in the form of a correction after strong growth. However, this is exactly what happened: after the completion of a short-term downward correction, American stock indices again moved to growth, and the dollar continued to strengthen.

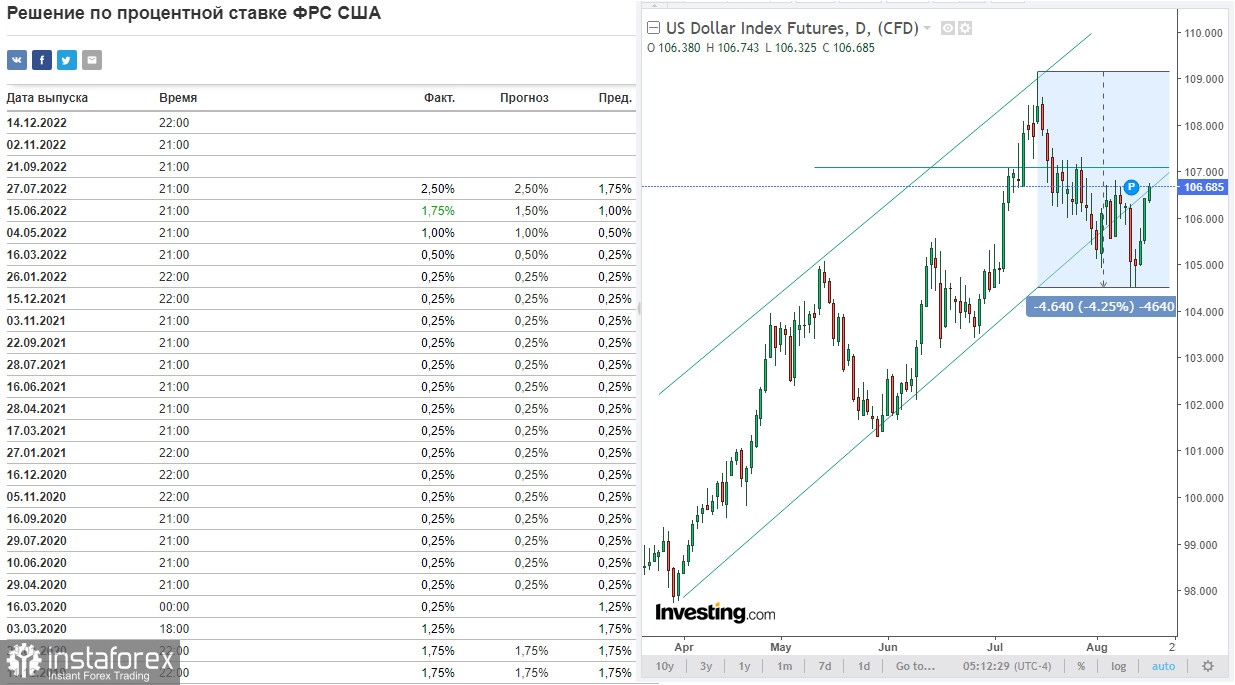

Today this continues to be the case, and growth of the DXY index resumed from the opening of the trading day. Thus, as of this writing, futures for the dollar index (DXY) are trading near 106.69, 26 points above the closing price of yesterday's trading day.

As you know, the dollar fell following the results of the past week. The reason for this was the weaker consumer price index (CPI), published last Wednesday.

As follows from the report of the US Bureau of Labor Statistics, the annual producer price index (PPI) in the US in July fell more than expected, to 9.8% from 11.3% in June, which was also below market expectations of 10.4%. The annual core PPI also fell to 7.6% in July from 8.2% a month earlier.

Weaker inflation data significantly dampened expectations for a larger Fed rate hike, putting pressure on the dollar.

Now the probability of a 75 bps Fed rate hike fell to 35% in September from 80% (before the publication of the CPI), according to the CME Group, which also affected the yield of US Treasury bonds, causing it to decline sharply.

Based on the weekly data on the jobless claims published on Thursday, which also turned out to be weaker, the DXY index made a new attempt to break through the local support level of 104.50, dropping to 104.52.

Nevertheless, Fed officials were quick to reassure market participants, saying it was too early to declare a "victory over inflation," which remains "unacceptably" high.

In particular, Minneapolis Fed President Neel Kashkari said he "does not see anything that would change" the need for the Fed to raise the discount rate to 3.9% by the end of the year and to 4.4% by the end of 2023.

According to Fed Chairman Jerome Powell, the US labor market and economy remain strong and are able to withstand the high pace of the monetary tightening cycle. As you know, the Fed has already raised interest rates four times this year, first by 0.25% in March, then by 0.50% and 0.75% in June and July. Usually, the Fed prefers to move in smaller steps, changing interest rates at its meetings by 0.25%.

The next Fed meeting will take place on September 20–21. Even if the Fed once again raises the interest rate by 0.25% or 0.50%, it will still confirm the firm intention of the Fed's leadership to overcome high inflation in the US, which remains at 40-year highs.

At a press conference following a July meeting that raised the rate by 0.75%, Powell said a "moderately tight monetary policy" was justified by current economic indicators, including high inflation, while also stressing another sharp rate hike in September.

Now market participants will carefully study the minutes from this Fed meeting in order to more accurately assess the likelihood of such an increase in September and the further intentions of the leadership of the US central bank. The publication of these protocols is scheduled for tomorrow at 18:00 (GMT).

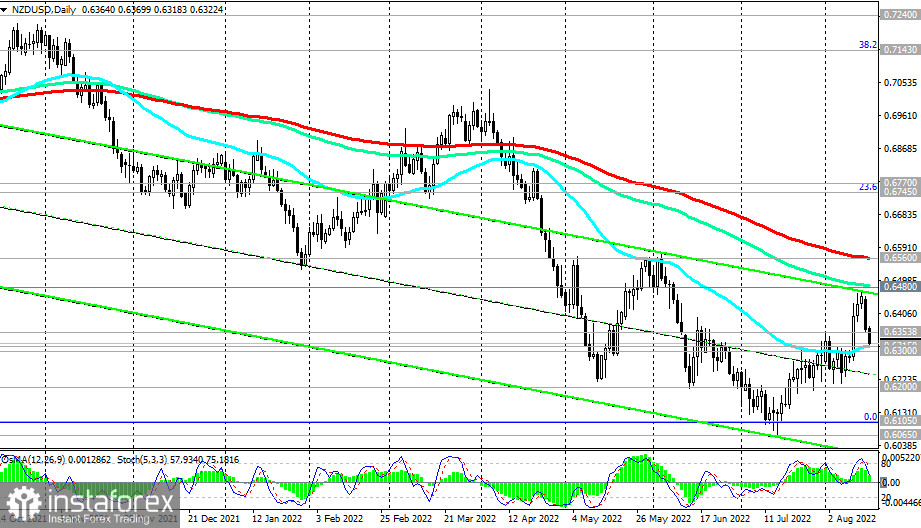

Also, tomorrow (at 02:00 GMT), the decision of New Zealand's central bank on the interest rate will be published, which will cause a sharp increase in volatility during the Asian trading session, primarily in NZD quotes.

The RBNZ may again raise the interest rate and speak in favor of a further increase in the interest rate at the next meetings. Currently, the RBNZ interest rate is 2.5%. Earlier, the RBNZ stated that the economy no longer needs the current level of monetary stimulus.

If the accompanying RBNZ statement signals a wait-and-see attitude, the New Zealand dollar is likely to come under pressure. However, the market's reaction to the RBNZ's decision on the interest rate in the current situation may turn out to be completely unpredictable.

As of this writing, the NZD/USD pair is trading near the 0.6325 mark, in the zone between important short-term levels, support 0.6300 and resistance 0.6358. Their breakdown in one direction or another will determine the further direction of the pair's dynamics. In general, the downward dynamics of NZD/USD prevails while the pair remains in the long-term bear market zone.

InstaForex analytical reviews will make you fully aware of market trends! Being an InstaForex client, you are provided with a large number of free services for efficient trading.